The fixed asset lifecycle refers to the various stages that a fixed asset goes through during its existence within an organization. It encompasses the acquisition, utilization, maintenance, and disposal of fixed assets. Here are the key stages of the fixed asset lifecycle:

Planning and Acquisition:

Asset Deployment and Utilization:

Maintenance and Upkeep:

Monitoring and Depreciation:

Asset Scrap, Disposal or Replacement:

Data and Reporting:

The fixed asset lifecycle is a continuous process that involves careful planning, monitoring, and decision-making to ensure efficient utilization, proper maintenance, and timely replacement or disposal of assets. Effective management of the fixed asset lifecycle helps organizations optimize asset value, control costs, comply with regulations, and make informed decisions regarding their asset portfolio.

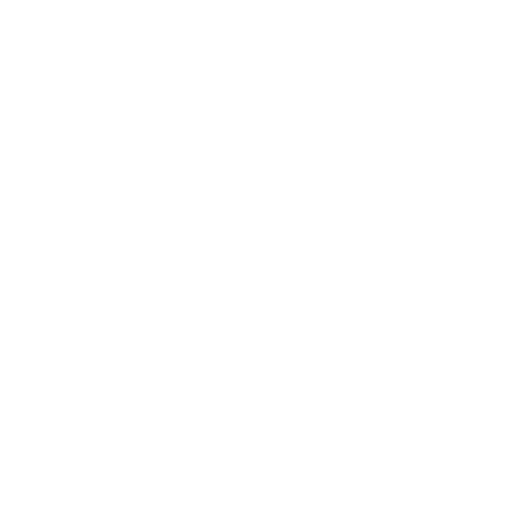

A fixed assets purchase invoice is a document that records the purchase of a fixed asset, such as land, buildings, machinery, or equipment. Unlike regular purchase invoices for consumable items, a fixed assets purchase invoice typically involves a significant amount of money and a long-term commitment from the company. Therefore, it requires more detailed information and processing.

A typical fixed assets purchase invoice includes the following information:

Fixed assets purchase invoices are typically processed and recorded by the accounting department of the company. The information is then used to calculate the depreciation expenses for the fixed asset over its useful life, which is important for accurately reporting the company’s financial position and performance.

![]()

A fixed asset transfer is a process of moving a fixed asset, such as machinery, equipment, furniture, or vehicles, from one department, location, or company to another. Fixed asset transfers can occur for various reasons, including restructuring, reallocation, replacement, and disposal. The transfer process involves updating the asset records to reflect the change in ownership, location, and condition.

The fixed asset transfer process typically involves the following steps:

Fixed asset transfers are essential for maintaining accurate fixed asset records and ensuring that the assets are being used effectively and efficiently. Proper documentation and record-keeping are necessary for compliance with accounting standards and tax regulations. It is important to follow established policies and procedures to ensure that fixed asset transfers are authorized, properly recorded, and effectively managed.

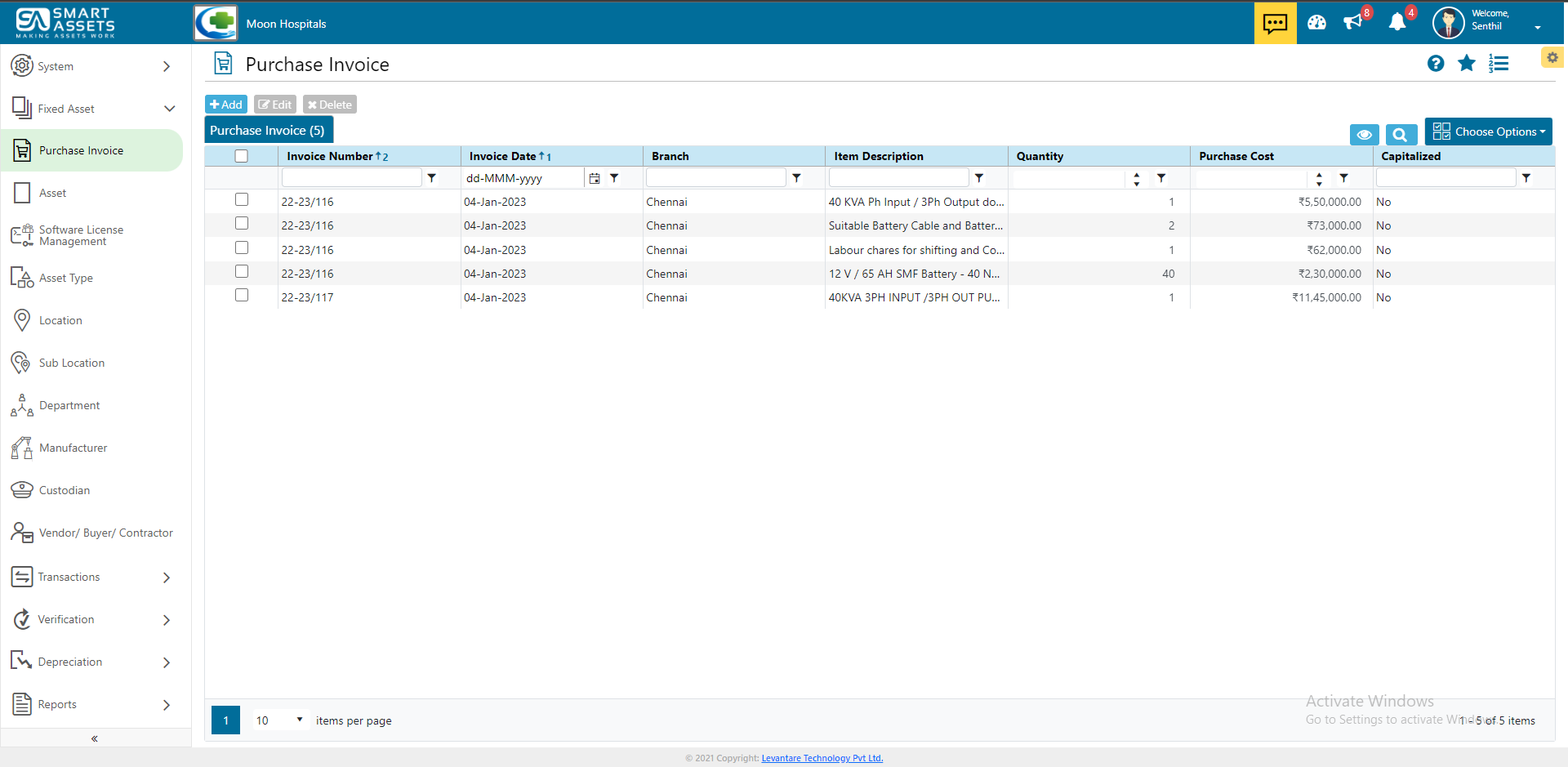

Asset scrap is the process of disposing of a fixed asset that is no longer useful or has reached the end of its useful life, include things like machinery, vehicles, or equipment that have reached the end of their useful life or have become obsolete. Fixed assets that are no longer needed can be sold, donated, or scrapped, depending on their condition and value. The process of asset scrap involves removing the asset from the accounting records, recording any proceeds from the sale or disposal, and properly disposing of the asset.

The asset scrap process typically involves the following steps:

Proper asset scrap management is important for maintaining accurate fixed asset records and ensuring compliance with accounting standards and tax regulations. It is essential to follow established policies and procedures to ensure that asset scrap is authorized, properly recorded, and effectively managed.

Effective management of asset scrap can also help organizations reduce costs, improve efficiency, and free up valuable resources for other purposes.

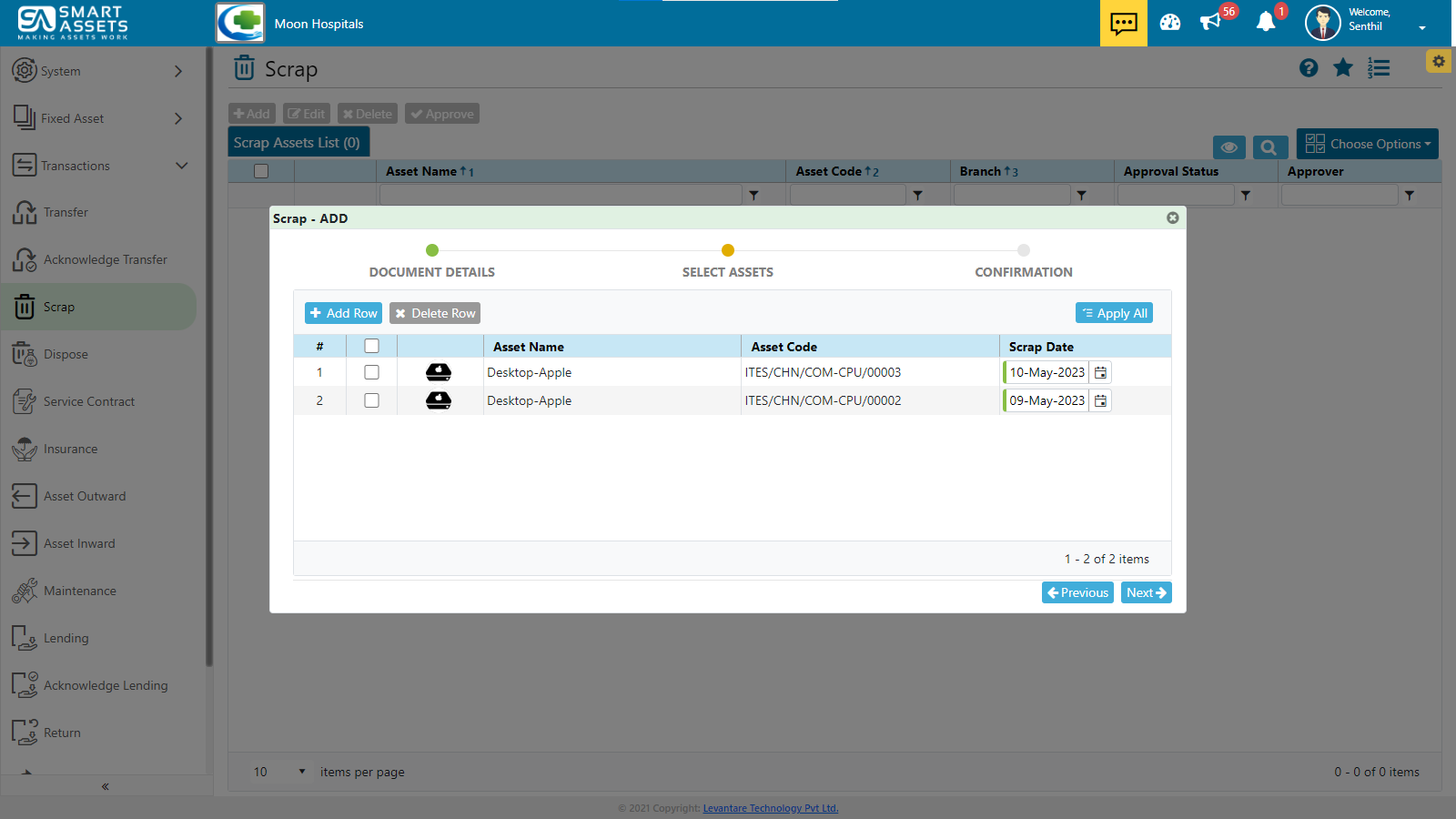

Asset disposal is the process of getting rid of a fixed asset that is no longer needed or useful to an organization. Disposing of an asset can involve selling it, donating it, scrapping it, or abandoning it. The process of asset disposal involves removing the asset from the accounting records, recording any proceeds or losses from the sale or disposal, and properly disposing of the asset.

The asset disposal process typically involves the following steps:

Proper asset disposal management is important for maintaining accurate fixed asset records and ensuring compliance with accounting standards and tax regulations. It is essential to follow established policies and procedures to ensure that asset disposal is authorized, properly recorded, and effectively managed. Effective management of asset disposal can also help organizations reduce costs, improve efficiency, and free up valuable resources for other purpose

In accounting and finance, “outward” can refer to several things, but in the context of fixed assets, “Outward” refers to the process of sending the fixed assets from the company to another party with specific reason, such as a customer or another company. There can be several reasons why a company may choose to move its fixed assets outward:

Overall, the decision to move fixed assets outward is based on the specific needs and circumstances of the company, and requires careful consideration of the potential benefits and risks involved.

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry’s standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged. It was popularised in the 1960s with the release of Letraset sheets containing Lorem Ipsum passages, and more recently with desktop publishing software like Aldus PageMaker including versions of Lorem Ipsum.

Fixed assets maintenance refers to the process of preserving and prolonging the useful life of fixed assets through regular inspections, repairs, and preventive maintenance activities. The goal of fixed assets maintenance is to minimize breakdowns, extend the useful life of the asset, and reduce repair costs.

Fixed assets maintenance typically involves the following steps:

Effective management of fixed assets maintenance can help organizations minimize downtime, reduce repair costs, and maximize the value of their fixed assets. It is essential to follow established policies and procedures to ensure that maintenance activities are scheduled, documented, and performed according to best practices. Regular maintenance can help extend the useful life of the asset, prevent unplanned downtime, and ultimately save the organization money over time.

A fixed assets service contract is an agreement between an organization or company and a service provider to provide maintenance and repair services for the organization’s fixed assets over a specified period. A fixed assets service contract typically includes the following details:

Fixed assets service contracts can provide organizations with several benefits, such as predictable maintenance costs, reduced downtime, and improved asset performance. They can also help organizations optimize their maintenance programs, ensure compliance with regulatory requirements, and free up resources to focus on core business activities. It is essential to carefully evaluate service providers and negotiate service contracts that meet the organization’s specific needs and objectives.

Fixed assets insurance is a type of insurance policy that covers the loss or damage of an organization’s fixed assets due to covered events, such as fire, theft, vandalism, or natural disasters. Fixed assets insurance policies typically cover a range of fixed assets, including buildings, machinery, equipment, and vehicles.

Fixed assets insurance policies can be tailored to meet the specific needs of an organization, and coverage can be adjusted based on the value and type of assets being insured. Some common types of fixed assets insurance coverage include:

Fixed assets insurance is an important component of risk management for organizations that rely on fixed assets to operate their business. It can help protect against the financial impact of unexpected events that could result in the loss or damage of fixed assets, and it can provide peace of mind to business owners and stakeholders. It is important to work with a reputable insurance provider and to carefully evaluate insurance policies to ensure that they meet the specific needs and objectives of the organization.

Fixed asset lending is a type of financing in which an organization borrows money using its fixed assets as collateral. Fixed assets include physical assets such as land, buildings, machinery, and equipment that have a long-term value and are not intended for sale in the normal course of business.

Fixed asset lending typically involves the following steps:

Fixed asset lending can be a useful tool for organizations that need to finance large investments in fixed assets but do not have the necessary capital on hand. It can provide access to capital at lower interest rates than other types of financing, such as unsecured loans or lines of credit. However, it is important to carefully evaluate the terms and conditions of the loan agreement and to ensure that the organization has the ability to repay the loan in full. Failure to repay the loan can result in the loss of the fixed assets used as collateral.

Fixed asset leasing or renting is a type of arrangement in which an organization obtains the use of a fixed asset, such as machinery or equipment, for a specified period of time in exchange for regular payments to the owner of the asset. This type of arrangement is also known as an operating lease.

Fixed asset leasing typically involves the following steps:

Fixed asset leasing can be a useful tool for organizations that need to use fixed assets but do not have the necessary capital to purchase them outright. Leasing can provide access to the latest equipment and technology, with the option to upgrade or replace assets at the end of the lease period. Additionally, leasing payments may be tax-deductible, depending on the tax laws in the organization’s jurisdiction.

However, it is important to carefully evaluate the terms and conditions of the lease agreement and to ensure that the organization has the ability to make regular lease payments throughout the duration of the lease. Failure to make lease payments can result in default and the loss of the fixed asset.

New #103, Eldams Road, Teynampet,

Chennai – 600018

27Q2+FW Chennai, Tamil Nadu

© 2024 Levantare Technology. All Right Reserved. Designed & Developed by Innov Touch Technologies Pvt Ltd.